Before 2017 fades into the past as a distant memory, I thought I might take a moment to review our financials for the year. We started tracking our money in September of 2016 so 2017 was the first full year where we tracked our money.

2017 Savings

2017 was a good year for savings. At the end of 2016 I published a post where I laid out our savings plan for 2017. When we originally made a FIRE plan in 2016 we aimed to save $120,000 a year. That seemed like a large number. It was also a number I pulled out of thin air, because at the time that we made our original plan we had just started tracking our finances, so I had no idea how much we could save. By the end of 2016 it became apparent that we could do $120,000 with ease. So, in the aforementioned post, I ever so bravely raised our savings goal to a whopping $160,000. How clueless was I? I had fewer clues than there are snowflakes in hell. We saved $317,965.74 in 2017.

You can read our monthly updates for 2017 or feast your eyes on this summary chart.

January 2017 was our strongest month of the year, while November was our worst.

We maxed out Mr. BITA’s 401k in January, and his company gave him his full match in that month too. My 401k was maxed out in June, with my company doing a ‘true-up’ of their matching contributions until August. By September we had maxed out all our Roth space – two backdoor Roths ($5,500 * 2) and one mega backdoor Roth ($27,000). Our HSA contributions were spaced out evenly all through the year. Mr. BITA’s company contributes $2,000 to our HSA account, and that is why January’s HSA bar is larger than the rest.

Next, let’s look at the data from the perspective of the source of our savings.

We save the entirety of our stock grants. These are a mix of Restricted Stock Units (RSUs) vesting and stocks from participating in an Employee Stock Purchase Plan (ESPP). Taxable contributions refers to money we save from our take-home paychecks.

Where We Spent Our Money

Next we take a look at our expenditures for 2017.

Mortgage (actually principal, interest, property tax and insurance), taxes and daycare make up 60.4% of our spending. The taxes in this chart are tax payments that we make over and above what is withheld by our companies (we owe estimated taxes primarily because of our RSUs and ESPPs, and also because of money that we have invested in India).

The ‘Everything Else’ category in the pie chart above does not actually exist in my sheets. Google Sheets stubbornly refused to label all 25 of my categories, so I lumped the 9 smallest categories into a single bucket. So the 7.5% ‘Everything Else’ slice includes gifts, shopping, child activities (dance class, swim class etc.), alcohol, entertainment (netflix subscription, tickets to the zoo, movie tickets etc.), house supplies (shampoo, detergent, toilet paper etc.), personal care (haircuts, massages etc.), gas and miscellaneous.

Expenses of note in 2017 include:

- Travel to Portugal, Croatia and two trips to Amsterdam.

- A trip to New Orleans that included my mother.

- I attended Fincon in Dallas.

- We went camping at the Henry Cowell State Park and at Yosemite.

- We had a host of houseguests in 2017. My mother stayed with us for 2 months at the start of the year, and half a month at the end of the year. My father visited for about 3 weeks. My in-laws, sister-in-law and niece visited for a week in April. My in-laws visited us a second time, and brought my nephew with them for a week in the summer.

- I had emergency hernia repair surgery in January of 2017 and another minor surgery in December.

- Our dog had expensive dental problems in April of 2017.

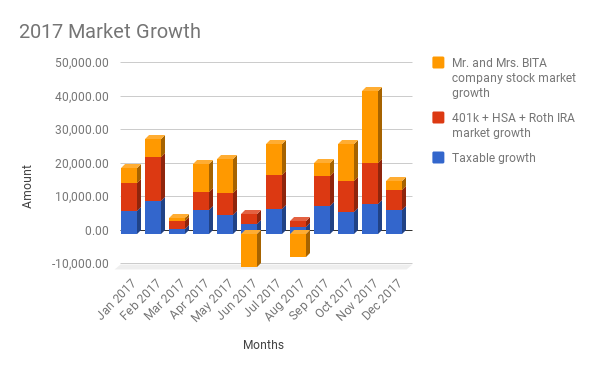

The Market in 2017

Mr. Stash, the third wheel of our TIIK family worked nearly as hard as we did in 2017. We made (unrealized gains) $229,085.15 in the market.

Our 401ks, HSA, Roths and taxable accounts all hold broad based index funds – the vast majority of which are Vanguard and Fidelity funds.

We do hold a fair chunk of company stock, but this is not part of some clever strategy. We spent years accumulating company stock when we did not know any better and selling it all off now during our peak earning years to invest in index funds instead would result in a very large tax bill. We no longer accumulate company stock – these days we sell as soon as our options vest. The plan is that once I retire and we drop into a lower tax bracket we will start to divest ourselves of these old holdings. In 2017 we were lucky enough to benefit from some significant growth in these holdings, but as the chart clearly shows, we are also subject to a fair bit of volatility because of them.

2017 Review: Lessons Learned

2017 was a year of tremendous growth for us financially, and not just because of the literal growth of our stash.

We learned that we are capable of saving far larger amounts that we had dreamed possible. The vast majority of our savings is a result of the fact that we make good money. But while we definitely tilt towards the income side as our weapon of choice to get to financial independence, we did not entirely neglect the expenses side of things. We stepped off the hedonic treadmill in various expense categories in 2017. For example, we ate out a lot less and have thus found that we are that much more excited when we do go out to eat. I learned a lot about churning and used credit card points to subsidize a lot of our travel. I joined and participate actively in my local Buy Nothing group.

All told, last year was a spectacular year financially for the BITA family. I am ever so grateful to be entering 2018, possibly my last year of corporate employment with the strong winds of 2017 at my back.

Congratulations on such a stellar year!

Thank you!

I fully expect to see a picture of smiley faces rolling around in bed with Mr. Stash one day. He is a big, big dude!

Hahahahah.

Love it! Way to flex your savings muscles in 2017!

Appreciate it Mrs. COD.

That is an amazing amount of savings. Wow. Can you beat it in 2018???

We will certainly try.

You had a budget of 190k for 2017, saved 318k, meaning you made 508k? And only paid 43k of taxes? You probably have a large outstanding tax liability, that 43k tax payment only covers California state taxes. You may owe another 150k in taxes, or am I missing something? Perhaps a huge portion of your savings resulted from RSU appreciation post-grant, and you haven’t realized those gains yet?

I’m not sure where you got your 190k number from, but no, that is not our budget. I’m also not sure where you got 43k from. We have paid far more in taxes than that number.

I echo the congratulations. That is fantastic!

Much appreciated.

Congratz on that impressive savings amount…! And kudos for keeping an eye on the cost side of the equation as well. It would rzally be easy to “only” save 1K less per month and spend that on food, drinks,… Focus on what matters and makes you happy.

The 25x (or 33x or whatever number you choose) rule makes keeping an eye on the costs relatively easy. 1k a more a month means 12k more a year and that translates (at 4%) to 300k more in the Stash, which at our rate of savings could mean another year of work. Nope, no thank you.